SJS Quarterly Outlook – July 2026

Each quarter, we create an outlook that covers topics including general investment market conditions, financial planning considerations, and SJS news.

Why Long-Term Advisor Relationships Matter More as Wealth Grows

There has never been more access to financial information to guide investment decisions, yet that information is not designed for the individual investor behind it.

How to Simplify a Financial Life That’s Grown Complex

As life grows, finances usually do too. More responsibilities, more accounts, more decisions, and more pressure to make the right calls can turn a once-simple financial life into something that feels harder to manage.

What Happens After the Sale? Planning Life After a Liquidity Event

While working within a business, owners live and breathe the business 24/7. Once a business is sold, whether to family, trusted employees, or to an outside third party, life for the owner may change dramatically.

Empowering Financial Literacy: Student Insights from SJS Shadow Program

At SJS Investment Services, we believe financial literacy is one of the most powerful tools you can develop early in life. When individuals build strong financial habits at a young age, they gain more than just knowledge - they can develop discipline, confidence, and long-term resilience.

Business Exit Planning Starts Earlier Than You Think

Business exit planning isn’t just about selling—it’s about readiness. Learn why early planning creates better outcomes and fewer regrets.

Why “Set It And Forget It” May Not Work For High‑Net‑Worth Families

In recent years, the rise of index funds has reshaped how many investors think about managing money. Low costs, diversification, and simplicity are real advantages – and within investment portfolios, they’ve proven effective over time. But in our experience, the idea of “set it and forget it” doesn’t typically translate well beyond investments.

Financial Surprises New Retirees Often Face

Most people spend decades preparing for retirement. They save consistently, invest diligently, and build an investment portfolio designed to grow over time to replace their paycheck one day.

Retirement Isn’t a Date: How to Plan for Income Across Every Phase

Retirement has long been treated like a finish line, but the truth is much different than that. It is a multi‑decade journey of living with purpose and meaning. The mosaic of your retirement may be composed of a mix of time spent with family and friends, travel, volunteering, and an active lifestyle.

Student Shadow Program Builds Financial Literacy Skills

This winter, we had the pleasure of hosting two students from Northview High School through our six-week financial literacy student shadow program in our Sylvania, Ohio office.

SJS Book Club: Why Small Habits Matter for Investing, Retirement, and Life

At SJS, we often talk about what it means to build a better life. While investing and financial planning play an important role, we know the foundation of a better life is much broader than simply making sound financial decisions. Living a more meaningful life often starts with small, consistent habits.

Stay On Target

Every January, Wall Street releases its newest flurry of S&P 500 year‑end predictions. And inevitably, we’re asked where we think the market is headed. At SJS, we certainly have opinions, but we don’t publish short-term market forecasts or build client portfolios around them.

Don’t Let Bubble Talk Burst Your Plan

Are valuations excessively high? Do record earnings justify selling? Headlines that stir fear are not new. Investors often get caught up in market noise, but recognizing that news headlines are often written to prioritize clicks over nuanced truth can reduce stress.

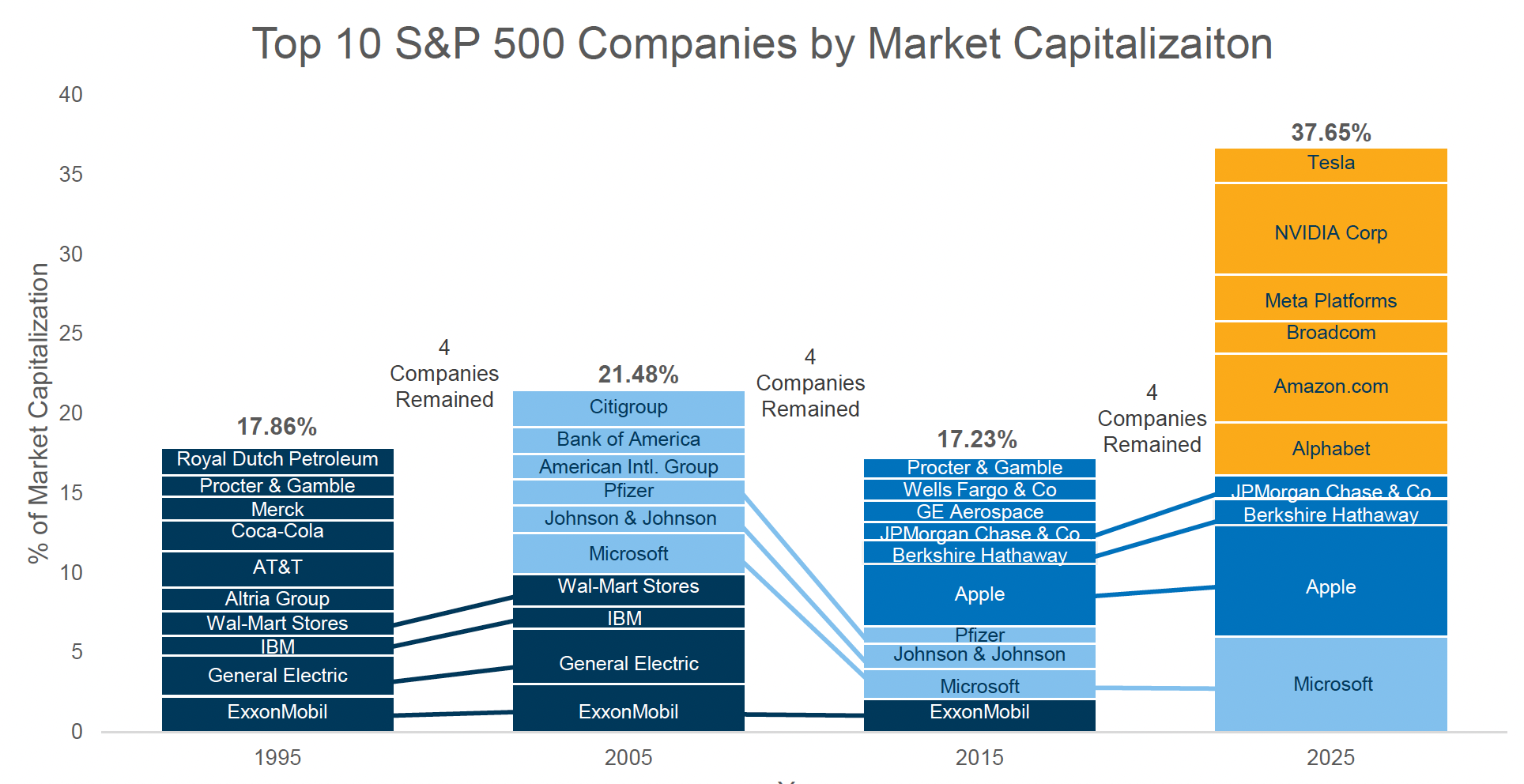

AOL to AI: How Innovation Keeps Reshaping Market Leadership

Do you remember when AOL was the internet? When hearing “You’ve got mail” felt like a small event, and logging on meant you were connected to the future?

Your Wealth in 2026: New Year, New Limits

The beginning of 2026 is a natural checkpoint to make sure your saving, gifting, and protection strategies still match the life you are living today. Your financial planning can benefit from a fresh look at the start of each year and we have a some actionable ideas to start the new year on the right foot, financially.

Imagine Peace of Mind

As we excitedly look forward to the year ahead, we remain deeply committed to empowering you to build a better life and providing the peace of mind you deserve.

SJS Quarterly Outlook – January 2026

Each quarter, we create an outlook that covers topics including general investment market conditions, financial planning considerations, and SJS news.

Important Financial Planning Numbers For 2026

As you look ahead to 2026, it’s easy to feel overwhelmed by all the new financial and tax updates. To make things simpler, we want to highlight the key numbers to keep on your radar this year.

From Capitol Hill to Main Street: How the Big Beautiful Bill Impacts Your Business

As we discussed in our last blog post, Congress passed the long-anticipated One Big Beautiful Bill Act (OBBBA). True to its name, this legislation covers a wide range of tax and financial provisions. And for business owners in particular, the impact is meaningful [1].

Walking the Tightrope: The Fed, the Market, and Your Bonds

Interest rates don’t always make headlines, but when they do, they tend to shake everything else. That’s because rates sit at the heart of the economy: they influence borrowing costs, savings yields, and business investment.