What's The (Gold) Rush?

Gold has delivered eye-catching gains in recent years, surging past $4,000 per ounce this year and headlining financial media with talk of safe havens, inflation fears, and geopolitical uncertainty.[1] This performance has increased investor enthusiasm, but history and research suggest caution.

At SJS, we believe investments should be grounded in fundamentals. Assets ought to generate earnings or possess inherent value beyond the hope of resale at a higher price. When the rationale for owning something is simply that someone else might pay more for it later, we’ve crossed into speculation - where value is propelled by hope or hype.

Gold is a unique asset. It doesn’t produce income like stocks or bonds. It doesn’t compound, doesn’t pay dividends, and for most investors, it has limited practical use. Its value is largely determined by sentiment by what someone else is willing to pay for it, which makes it inherently different from productive assets.

The supply of gold remains relatively stable; demand is less so. Gold supply is driven by mining and recycling, with lab-grown gold contributing in rare cases. Advances in lab-grown gold may increase supply in the future, with the impact on prices difficult to predict. Investor psychology, macroeconomic fears, and geopolitical tensions can all drive demand, and therefore price, in unpredictable ways. This volatility creates a mismatch with the narrative often attached to gold: that it is a reliable hedge against inflation. But historically, gold has not consistently behaved as an inflation offset. Its price movements are often more volatile than inflation itself, and its correlation with inflation is far from perfect.

Comparatively, the long-term value of stocks is driven by the profits and cash flows of the underlying businesses. The long-term value of fixed income is driven by contractual payments with businesses and other entities in exchange for providing financing. We think that there are more robust economic theories underlying why stocks and fixed income will increase over time than for gold.

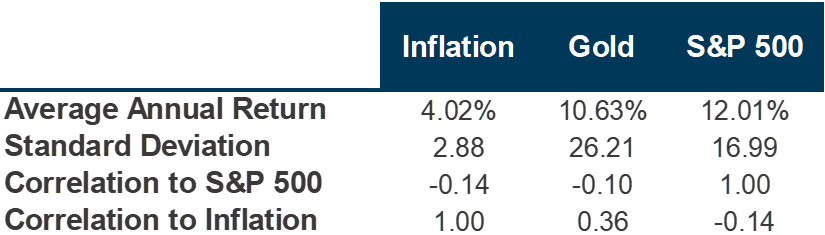

Since 1969, gold has lagged U.S. stock returns. Its annualized return has been lower than the S&P 500 Index, while its standard deviation, a measure of risk, has been notably higher from April 1969 to October 2025.[1]

Source: Morningstar. Data spans from 4/30/1969 – 10/31/2025 for average annual return, standard deviation, and correlations. Inflation is represented by the US BLS CPI All Urban SA. Gold is represented by the LBMA Gold Price PM USD, the official benchmark price for gold set in US dollars each afternoon in London, used globally to standardize gold pricing. S&P 500 is represented by the S&P 500 TR Index. See Important Disclosure Information.

Gold is not new - it has been used as a currency and investment asset for thousands of years. Based on a 2025 study by Claude Erb and Campbell Harvey, gold has held its after-inflation value for the last 2,000-plus years; at the same time, its after-inflation purchasing power has not changed much, which implies a real return around 0%.[2]

This 2,000-plus year performance is in contrast to the past few decades, when gold has performed well. Even the recent performance has been uneven - a gold investor would have had to endure nearly 25 years of cumulative losses from the early 1980s to the mid 2000s. While no one knows what will happen, historical precedent does not lead us to be optimistic about the future prospects of gold.

Source: Morningstar. Gold is represented by the LBMA Gold Price PM USD, the official benchmark price for gold set in US dollars each afternoon in London, used globally to standardize gold pricing. The SPDR® Gold Shares ETF (GLD) was the first gold ETF launched in the U.S. on November 18, 2004. See Important Disclosure Information.

While gold has hedged against inflation and has preserved purchasing power for over 2,000 years, few of our clients have such a long investment horizon. Over shorter periods, gold has exhibited volatility comparable to stocks. Even though direct ownership of gold may not be our preferred strategy, there are several indirect approaches that can help create exposure to gold, serving as useful portfolio diversifiers during periods of speculation.

One option is to invest in companies connected to gold supply and demand, such as mining firms. In a well-diversified portfolio, ownership of these companies is typically already included as part of broader market exposure. Another approach is to access gold exposure through alternative investment strategies - such as buying & selling gold futures within a diversified investment strategy as well as providing price certainty to investors through insurance-like instruments - that have historically been profitable. These methods can be particularly beneficial in times of heightened inflation or when inflation expectations are rising.

When considering investing in gold, it is important to remember historical lessons. During the California Gold Rush in the mid-1800s, the reported wealthiest individual in California was not a gold miner, but a businessman who profited from selling mining supplies and publishing news about the rush.[3][4] While gold remains a time-tested store of value, we believe that successful investing requires a balanced approach that considers both historical insights and practical portfolio strategies that are not solely focused on golden opportunities to strike it big.

Important Disclosure Information & Sources:

[1] Source: LBMA. Gold is represented by the LBMA Gold Price PM USD, the official benchmark price for gold set in US dollars each afternoon in London, used globally to standardize gold pricing.

The S&P 500 TR Index tracks the price changes of 500 leading publicly traded US companies.

Inflation is represented by the US BLS CPI All Urban SA, which measures the average change over time in the prices paid by urban consumers for a market basket of goods and services in the US, seasonally adjusted.

[2] “Understanding Gold”. Claude B. Erb and Campbell R. Harvey, 07-Oct-2025, papers.ssrn.com.

[3] “California Gold Rush”. History.com Editors, 28-May-2025, history.com.

[4] “Samuel Brannan: Gold Rush Entrepreneur”. PBS, pbs.org.

Past performance does not guarantee future results. Diversification neither assures a profit nor guarantees against a loss in a declining market. There is no guarantee investment strategies will be successful. Past performance is no guarantee of future results.

Indices are not available for direct investment. Their performance does not reflect the expenses associated with management of an actual portfolio. Index performance is measured in US dollars. The index performance figures assume the reinvestment of all income, including dividends and capital gains.

MarketPlus® Investing models consist of registered investment companies. Investment values will fluctuate, and shares, when redeemed, may be worth more or less than original cost.

Statements contained in this document that are not statements of historical fact are intended to be and are forward looking statements. Forward looking statements include expressed expectations of future events and the assumptions on which the expressed expectations are based. All forward looking statements are inherently uncertain as they are based on various expectations and assumptions concerning future events and they are subject to numerous known and unknown risks and uncertainties which could cause actual events or results to differ materially from those projected.